Choosing a retirement plan can be quite the undertaking due to the significant impact it can have on the quality of life you will live during retirement. Today, Roth retirement options are becoming more popular among professionals such as medical practitioners and business people. The rise in popularity of Roth options, such as Roth IRAs and Roth 401(k)s, over traditional retirement options is due to the tax-free earnings advantage.

The tax-free earnings advantage

In both Roth IRA and Roth 401(k) retirement plans, you will make your contributions after taxes. This means that you won’t be deducting your contributions from your taxable income when filing your taxes. This is contrary to traditional retirement options where you deduct your contributions from your taxable income. With Roth options, down the road when you are beginning your retirement, you can take out your earnings tax-free. It is this tax-free advantage on the distributions from the Roth option that is attracting professionals and business people to these retirement plans.

Are there any differences between the Roth IRA and Roth 401(k)?

Though the Roth IRA and the Roth 401(k) operate similarly, they are quite different from one another. First and foremost, a Roth IRA is an individual retirement account set up by a individual. A Roth 401(k) is only available through a qualified retirement plan, typically offered from your employer. Below are five other areas in which these two options, that share the same tax-free earning advantage, differ.

Click HERE to download a free PDF summary of the points outlined in this article.

-

Limits to contributions

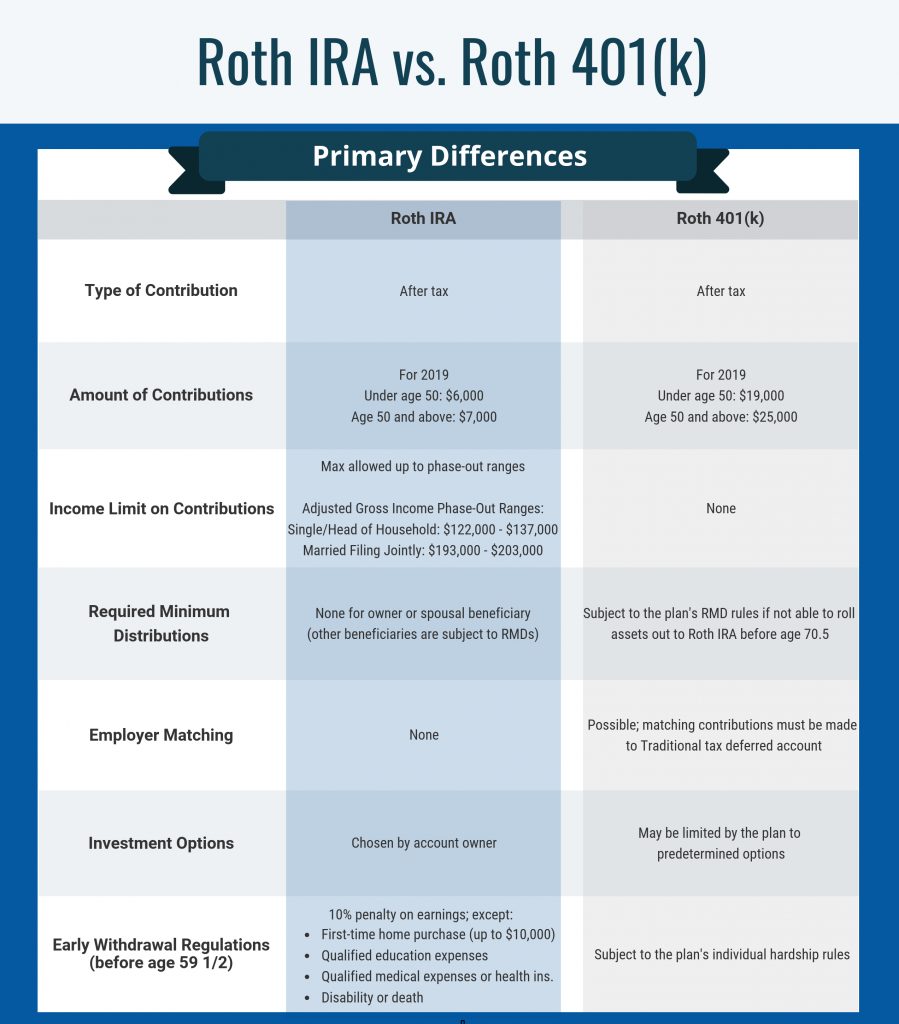

The most notable difference between the two retirement plans is the contribution and income limit. You should know that almost all retirement plans, even traditional options, have these limits. Keep in mind the limits can change from year to year.

The Roth 401(k) has a higher contribution limit as compared to the Roth IRA. In a Roth 401(k) retirement plan, you are allowed to save up to $19,000 every year if you are under the age of 50, according to the 2019 guidelines. In the year you turn 50 years of age and thereafter, your contribution limit rises to $25,000 every year.

On the other hand, in a Roth IRA, you are limited to making contributions of up to $6,000 every year if you are under the age of 50. Your contribution limits rise to $7,000 every year if you are age 50 and above.

When it comes to income limitations, only the Roth IRA has them. The ability to make the maximum contribution is phased out starting at $122,000 and completely phased out at $137,000, if filling single or head of household in 2019. The range is $193,000 to $203,000 for married filing jointly.

However, Roth 401(k) accounts are not subject to any income limitations.

-

Required minimum distribution

Required minimum distributions in simple terms are the minimum amount you are required to withdraw from your retirement account each year when you reach 70.5 years old.

For Roth IRAs, there are no required minimum distributions for your retirement account until the end of your life. If you pass away, your spouse will also have the benefit of not needing to take any minimum distributions. Additionally, they will not have to pay any taxes for your retirement saving. These benefits only extend to your spouse and no one else. If the beneficiary of your Roth IRA is someone other than your spouse, they will be subjected to required minimum distributions.

On the other hand, if you have a Roth 401(k) account, you will be subject to your retirement plan’s required minimum distributions. However, if you are eligible, you could roll your Roth 401(k) assets out of your qualified plan and into a Roth IRA prior to 70.5 and avoid the plan’s required minimum distributions.

-

Employer matching

Another consideration when weighing which is the best choice for you is if your employer offers any type of matching contribution into your 401(k) plan. Employer matching is where an employer can make contributions to your retirement plan matching what you contributed in full or up to a certain percentage. As an employed professional, you might simply call this free money. The contributions from your employer could significantly increase your savings by the time you retire.

If you are contributing to a Roth 401(k) plan, you have the possibility of benefiting from your employer matching your retirement contributions. You should know that what your employer contributes towards your retirement plan will be placed in a traditional tax deferred account.

The Roth IRA is an individual arrangement where you put your own after-tax money away for retirement savings.

-

Investment options

You might want to use your retirement savings to make investments in either stocks or bonds. A Roth IRA gives you, as the account holder, a lot more flexibility when it comes to investment choices. With a Roth IRA, you can choose where you want to invest your savings and how much of it you want to invest.

On the other hand, if you have a Roth 401(k) plan, you may be limited in how you can use the funds that you contribute to your retirement account to make investments. In some cases, your only option is to choose from a predetermined set of investment options offered by your employer’s retirement plan.

To enjoy the best of both worlds, you can start maximizing your contributions in a Roth 401(k) plan to take advantage of your employer’s matching. Once you have maximized your retirement savings in this plan, you can begin contributing to a Roth IRA and start making investments. This way, you will be able to have control over at least some of your retirement funds and investments.

-

Early withdrawal regulations

In both the Roth 401(k) and Roth IRA, early withdrawals (before age 59 ½) may be allowed, but the 401(k) plan document and IRS regulations will determine the parameters around these withdrawals. These are known as hardship rules and are defined by the plan document that governs the 401(k) plan. Despite this, you will still be subjected to an early withdrawal penalty on earnings, which is usually 10% of the money withdrawn. You do not have to pay taxes for any withdrawals made.

The Roth IRA plan stands out here, as it allows you to make early withdrawals under special circumstances without having to pay the early withdrawal penalty. These circumstances include a first-time home purchase (up to $10,000), qualified education expenses, unreimbursed medical expenses or health insurance if you are unemployed, or if due to a disability or death. In these circumstances, despite being under 59 ½ years old, you won’t have to pay any early withdrawal penalties.

Which is better: Roth IRA or Roth 401(k)?

There is no definite answer to this question as both the Roth IRA and Roth 401(k) have their benefits and downsides. Which retirement account suits you best entirely depends on both your current and future needs and what you aim to achieve. Despite this, you should keep in mind that the Roth 401(k) account option is only available if offered by your employer.

If you are a high earner, and you want to make significant contributions towards your retirement, the Roth 401(k) is best for you. This is because this account has no income limitations and allows for higher contributions. The higher contributions are close to triple what is allowed for a Roth IRA account, and this will make a massive difference in the amount you save in the long run.

If you want to enjoy more flexibility with the money that you have saved and choose your own investment options, you should opt for a Roth IRA. If you make wise investments, you can grow your savings effectively with this option. This account also has no set required minimum distributions and is more favorable if you plan to leave your account to an heir.

Can you take both options?

Yes, you can. This is as long as you meet the income limitations of the Roth IRA option. If you can’t manage to hit the contribution limits of both accounts, you should contribute to the Roth 401(k) first, if available, to benefit from any available employer’s matching of your contribution and increase your savings rapidly.

You will benefit the most if you start saving for your retirement as early as possible. The earlier you start, the more money you are likely to have when you transition into retirement. If you decide to invest your retirement savings, be wise about it.

Dean Investment Associates, LLC (“DIA”) and Dean Financial Services, LLC (“DFS”) are each a registered investment advisor with the SEC and wholly owned subsidiaries of C.H. Dean, LLC. Dean Capital Management, also an investment advisor registered with the SEC, serves as the sub-advisor for DIA. Dean Capital Management is an affiliate of C.H. Dean, LLC. Readers should note that utilizing a Roth IRA or Roth 401(k) does not guarantee a profit nor eliminate the risk of loss.